Paul Stirling is an independent writer, specialising in global trade and finance

In an era of geopolitical tension, rapid technological disruption, and shifting capital flows, international financial centres (IFCs) remain the indispensable engines of the global economy. These hubs channel trillions in cross-border investment, foster innovation in fintech and AI, and provide sophisticated risk management tools. Yet they face constant pressure—from regulatory crackdowns and transparency demands to competition from rising regional players and the accelerating pace of digital transformation.

According to the Global Financial Centres Index 391 (GFCI 39), published by Z/Yen in March 2026, the landscape shows remarkable stability at the top alongside dynamic shifts lower down. New York retains the crown, followed closely by London, Hong Kong, and Singapore.

Dubai has surged to 7th place—its highest ranking ever—while Tokyo re-enters the top 10. San Francisco holds 5th, with Shanghai (6th) and Shenzhen (9th) underscoring Asia’s strength. Overall ratings declined modestly across most centres amid global uncertainties, but connectivity, innovation, and regulatory predictability increasingly drive competitiveness.

This article examines the ecosystem from dominant global centres to dynamic regional hubs and specialised offshore jurisdictions. We analyse their respective strengths and weaknesses, incorporate executive perspectives from key players, and explore how offshore finance continues to thrive amid scrutiny, evolving from traditional tax planning toward compliance, innovation, and specialised services.

The enduring NY-London axis

New York and London form the traditional backbone of global finance, often referred to as the NY-LON axis. Together, they dominate wholesale markets, capital raising, derivatives, foreign exchange, and innovation, handling a disproportionate share of global transactions despite multipolar pressures.

New York (Wall Street) stands unrivalled in capital market depth. Home to the NYSE and Nasdaq, it benefits from the US dollar’s reserve currency status, unparalleled liquidity in Treasuries and equities, and deep synergies with Silicon Valley’s tech ecosystem. Institutional investors, private equity giants like Blackstone and KKR, and hedge funds cluster here, drawn by a robust legal framework (common law) and regulatory oversight from the SEC and Federal Reserve.

Strengths include unmatched scale—US equity markets represent roughly 40-50% of global market capitalisation in many metrics—talent attraction from Ivy League universities, and a culture of risk-taking that fuels disruptive innovation. Private equity and venture capital deployment remain world leading.

However, challenges are significant: exorbitant real estate and living costs in Manhattan, heavy regulatory burdens (Dodd-Frank, evolving SEC rules on climate disclosure and crypto), political polarisation, and vulnerability to US domestic policy shifts or global shocks like interest rate volatility.

London maintains its position as Europe’s premier international hub despite Brexit. It leads in foreign exchange (daily turnover often exceeding $2 trillion pre-adjustments), derivatives, insurance (via Lloyd’s of London), and crossborder banking. English common law, time-zone advantages (bridging Asia and the Americas), and a multilingual talent pool from the Commonwealth provide enduring edges.

The City and Canary Wharf continue attracting fintech innovators through the FCA’s regulatory sandbox, which has supported hundreds of trials in payments, crypto, and AI-driven services.

Post-Brexit frictions persist, including reduced EU passporting rights, talent mobility hurdles, and some relocation of euro-clearing business. High operational costs and competition from Frankfurt, Paris, and Dublin add pressure. Yet London’s adaptability—evident in its fintech leadership and green finance initiatives—keeps it resilient.

Professor Michael Mainelli, Chairman of Z/Yen, notes the concentration at the top: “The significant gap in ratings between the leading four centres and the rest implies there is no paradox of increasing concentration on fewer safe centres during a period of increasing deglobalisation.”

International financial centres, including their vital offshore components, continue to underpin global prosperity. While challenges from geopolitics, regulation, and technology persist, their adaptability suggests a resilient future

Asia’s rising powerhouses

Hong Kong (3rd) serves as a critical bridge between China and Western markets, excelling in IPOs, RMB internationalisation, and stock connect schemes. Its low-tax regime, common law system, and deep liquidity in equities and bonds are core strengths.

However, US-China tensions, the National Security Law, and capital flow restrictions introduce uncertainty. Hong Kong has responded with fintech and wealth management pushes, maintaining strong connectivity.

Singapore (4th) emphasises stability, wealth management, and fintech. Pro-business policies, world-class infrastructure, political predictability, and strict regulation make it a preferred treasury and asset management hub for Southeast Asia and beyond. It punches above its weight in sustainable finance and digital assets.

Limitations include a small domestic market and reliance on expatriate talent, though initiatives like the MAS sandbox mitigate this. Singapore’s rise reflects Asia’s broader shift toward multipolarity.

Regional contenders: Dubai’s meteoric rise and others

Regional centres gain ground in a multipolar world. Dubai, via the Dubai International Financial Centre (DIFC), climbed to 7th globally in GFCI 39. HE Essa Kazim, Governor of DIFC, commented: “Dubai’s remarkable progress in the Global Financial Centres Index is an outstanding milestone that highlights the Emirate’s ambitious vision and expanding influence on the international financial stage. Anchored by DIFC’s world-class infrastructure and forward-looking regulatory environment, we continue to strengthen Dubai’s position as the region’s leading global financial hub.”

Pros include zero-tax zones, 100% foreign ownership, modern infrastructure, and a strategic location. Growth in Islamic finance, fintech, hedge funds, and family offices is robust, backed by the D33 agenda targeting top 4 status by 2033. Challenges are regional risks, expat talent dependence, and maturing regulation.

Other contenders include Frankfurt (eurozone banking, green finance), Shanghai/Shenzhen (China’s domestic depth with capital controls), Mumbai’s GIFT City (India’s emerging hub), and rising spots like Astana or Johannesburg.

Offshore finance: specialisation and scrutiny

Offshore financial centres (OFCs) primarily serve non-residents, offering tax neutrality, asset protection, and flexible structures. They manage tens of trillions in global hedge funds, captive insurance, private wealth, and special purpose vehicles—assets estimated in the $13 trillion+ range for offshore financial wealth alone in recent analyses, with broader fund and corporate structures far larger. Modern OFCs emphasise compliance, innovation, and specialisation while meeting OECD, FATF, and EU standards.

The Cayman Islands leads in hedge funds and structured finance. With no direct taxes and English common law, it hosts the majority of global hedge funds and private funds (over 30,000 entities, with assets under management exceeding $8-10 trillion in recent estimates). Regulation by CIMA is sophisticated, and recent tokenisation rules enhance its digital edge.

British Virgin Islands (BVI) excels in company formation (hundreds of thousands of active entities), fintech, and digital assets. “BVI has a long track-record of promoting digital innovation and leveraging the full power of digital capability… Initiatives like the fintech sandbox are helping to stimulate innovation… The ability to embrace digital innovation will be crucial to a sustainable, post-pandemic economic recovery.” BVI Finance has highlighted. BVI’s Incubator Fund and progressive virtual asset guidance support startups while maintaining compliance via systems like BOSSs.

Guernsey strengthens its role in private wealth, trusts, funds, and sustainable finance. As a leading international finance centre, it offers specialist expertise in green and natural capital funds, channelling billions into climate projects. Its stable regulatory environment, proximity to Europe, and focus on substance make it attractive for family offices and ESG-aligned structures. Guernsey Finance promotes innovation across private equity, insurance, and pensions, with strong UK linkages (eg. significant capital flows supporting UK infrastructure).

Bermuda dominates insurance, reinsurance, and fintech. The Bermuda Fintech Advisory Board captures its approach: “Companies who are looking for a world class jurisdiction with a forward-thinking government that welcomes entrepreneurs… can find in Bermuda the jurisdiction that can make that idea a business reality.” Its Digital Asset Business Act (DABA), sandbox licensing, and Currency Standard Initiative position it at the cutting edge of digital assets, insurtech, and on-chain innovation, building on its re/insurance legacy.

Switzerland (Zurich/Geneva) upholds private banking excellence and neutrality, adapting to CRS/AEOI while excelling in wealth protection and asset management. Luxembourg leads EU fund domiciliation (UCITS/AIFs) with passporting advantages.

General advantages of offshore finance:

- Optimised tax planning and earnings retention for legitimate structures.

- Superior asset protection from creditors, litigation, and political risks.

- Privacy within robust compliance frameworks (beneficial ownership registers).

- Regulatory efficiency and specialist expertise (eg. BVI companies for holding structures, Bermuda captives for insurance, Guernsey trusts).

- Diversification, innovation in digital assets/sustainable finance, and access to global networks.

Drawbacks:

- Reputational risks and de-risking by some onshore banks.

- Elevated compliance/maintenance costs (FATCA, CRS, economic substance rules).

- Ongoing transparency pressures and blacklisting threats.

- Potential for misuse (though AML/CFT regimes have strengthened significantly).

- Complexity requiring expert advice.

Offshore finance has evolved dramatically since 2008 and the Panama Papers. Centres like Cayman, BVI, Guernsey, and Bermuda now largely meet or exceed international benchmarks on transparency while preserving efficiencies. Offshore assets have grown substantially as focus shifts to regulatory arbitrage, service excellence, and technology. Hybrid onshore-offshore strategies often yield optimal outcomes.

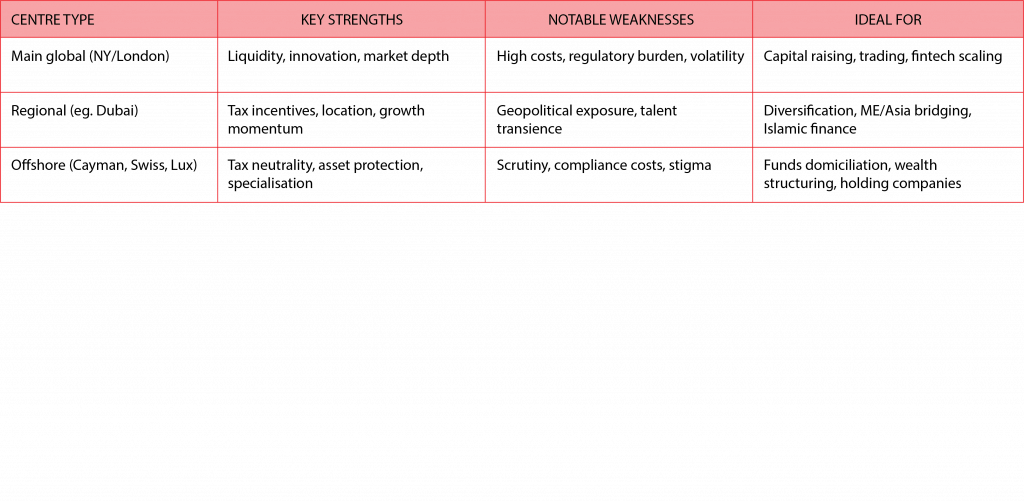

Figure 1. Comparative pros and cons: choosing the right hub

Technology, sustainability, and the future outlook

AI-driven trading, tokenisation, blockchain, and confidential computing reshape competition. Main centres dominate high-frequency and institutional flows, while OFCs adapt nimbly (eg. Cayman tokenisation, Bermuda’s on-chain ambitions, BVI sandboxes). Sustainable finance grows critical—Guernsey’s Green Fund regime and Bermuda’s ESG frameworks exemplify leadership.

GFCI data underscores the rising importance of the Global Innovation Index, government effectiveness, cybersecurity, and human capital. For businesses/investors, they need to adopt hybrid models, diversify jurisdictions, monitor AI/blockchain/sustainable opportunities, and prioritise substance. Policymakers should foster innovation alongside transparency to reduce systemic risks. Centres must invest in talent, infrastructure, and partnerships (eg. Cayman-London-Singapore-Dubai links).

In conclusion, international financial centres, including vital offshore components, underpin global prosperity. Challenges from geopolitics, regulation, and technology persist, but adaptability—exemplified by Dubai’s ascent, BVI’s fintech push, Bermuda’s insurtech/digital leadership, Guernsey’s sustainable wealth expertise, and the enduring NY-London-Asia axis—suggests a resilient future. Those who innovate, connect, and balance efficiency with responsibility will thrive toward 2030 and beyond.

Endnotes

1. GFCI 39 Report (Z/Yen, March 2026).